Investing in research and development (R&D) is key to increasing innovation, productivity and competitive advantage. It is beneficial for businesses and beneficial for the economy of our country.

What is the R&D Tax Incentive?

The R&D Tax Incentive provides targeted, generous and easy to access support for eligible R&D activity. The R&D Tax Incentive, which has replaced the R&D Tax Concession since the 1st of July 2011, offers research and development tax offsets designed to encourage more companies to engage in R&D. Entitlement to the program is broad-based, therefore it is open to any business of any size that is conducting eligible R&D activities.

The benefits of the program are:

- a 45 per cent refundable tax offset to eligible entities with an aggregated turnover of less than $20 million per annum;

- a non-refundable 40 per cent tax offset to all other eligible entities.

- The aim of the R&D Tax Incentive is to:

- increase competitiveness and boost productivity across the Australian economy;

- promote businesses to conduct research and development activities that may not otherwise have been conducted;

- offer companies more predictable, less complex support; and

- provide a greater incentive for small businesses to conduct research and development.

Despite all the advantages, research conducted by R&D Tax Specialists Swanson Reed has shown that 75% of eligible small businesses in Australia could claim the R&D Tax Incentive but don’t.

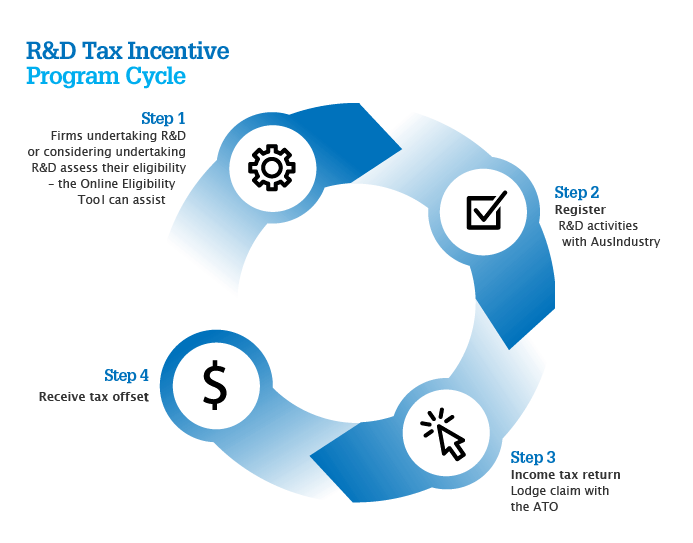

How does the program work?

Before applying to register for the R&D Tax Incentive each year, companies can self-assess their eligibility. The AusIndustry Online Eligibility Tool is designed to help businesses to assess whether their R&D activities are eligible for the R&D Tax Incentive.

Once eligibility is confirmed, companies must keep records with regards to eligible activities they have conducted and related expenses they wish to claim.

Companies will register their eligible R&D activities with AusIndustry and claim the tax offset in their company tax return through the Australian Taxation Office.

Local R&D activities

Normally only R&D activities conducted in Australia qualify for the R&D Tax Incentive. However, R&D activities conducted overseas qualify if Innovation Australia makes a finding that the activities meet certain conditions (i.e. section 28D of the Industry Research and Development Act 1986). Companies must apply for a finding about overseas activities before the end of the income year in which the activities were conducted.

Definitions:

- Eligible Entities

Only ‘R&D entities’ can register research and development activities and claim R&D tax offsets. You are an R&D entity if you are a corporation that is:

- incorporated under an Australian law; or

- incorporated under foreign law but an Australian resident for income purposes; or

- incorporated under foreign law and:

- a resident of a country with which Australia has a double tax agreement, including a definition of ‘permanent establishment’; and

- carrying on business in Australia through a permanent establishment as defined in the double tax agreement.

2. Core R&D activities

Core R&D activities are experimental activities:

- whose outcome cannot be known or determined in advance on the basis of current knowledge, information or experience, but can only be determined by applying a systematic progression of work that:

- is based on principles of established science; and

- proceeds from hypothesis to experiment, observation and evaluation, and leads to logical conclusions; and

- that are conducted for the purpose of generating new knowledge (including new knowledge in the form of new or improved materials, products, devices, processes or services).

None of the following activities are core R&D activities: market research, market testing or market development, or sales promotion (including consumer surveys).

Activities that are not core R&D activities may be eligible as supporting R&D activities.

3. Supporting R&D activities

Supporting R&D activities are activities directly related to core R&D activities. However, if an activity: a. is an activity referred to in the core R&D activities exclusions list; or

b. produces goods or services; or

c. is directly related to producing goods or services; the activity is a supporting R&D activity only if it is undertaken for the dominant purpose of supporting core R&D activities.

How to lodge a claim

The 30th of April of each year is the deadline to claim the R&D Tax Incentive for eligible activities conducted during the year ended 30 June of the previous year (i.e. last financial year).

Any companies seeking to lodge claims should take action before the 30th of April to ensure their activities are adequately assessed and described within their registration applications.

This includes the need to provide detail of:

- the specific Core experimental activities undertaken during the previous financial year;

- observations and conclusions of the experimental activities;

- why knowledge gained from the experimental activities is new;

- how any Supporting activities contribute to a corresponding Core activity.

What does the R&D Tax Incentive mean for the cosmetic industry?

This program is quite unique. It’s a great opportunity for Australian companies to invest in their own products or services and get up to 45% cash back on their investment when they lodge their next tax return (i.e. if their aggregated turnover is less than $20 mil per annum). The incentive is open to any industry including cosmetic and personal care companies. What research and development activities would or could your company conduct if they could get back nearly half of the money they spend? Is there any R&D that would really give your products a competitive advantage, but you always thought you couldn’t entirely afford it? Companies seeking to pursue this opportunity are encouraged to check eligibility, and then talk to their accountant or R&D Tax Specialist about taking advantage of the R&D Tax Incentive. For a small effort there might be quite a lot to be gained.

Sources: